The Role of Deductibles in Insurance: A Balanced Perspective

Insurance can sometimes feel overwhelming, with its complex terms and fine print. One of the most important—yet often misunderstood—concepts is the deductible. While it may seem like just another number on your policy, deductibles play a crucial role in how insurance works, affecting both your coverage and your wallet.

In this article, we’ll explore what deductibles are, why they exist, and how they influence your insurance experience—all in a straightforward, calm manner.

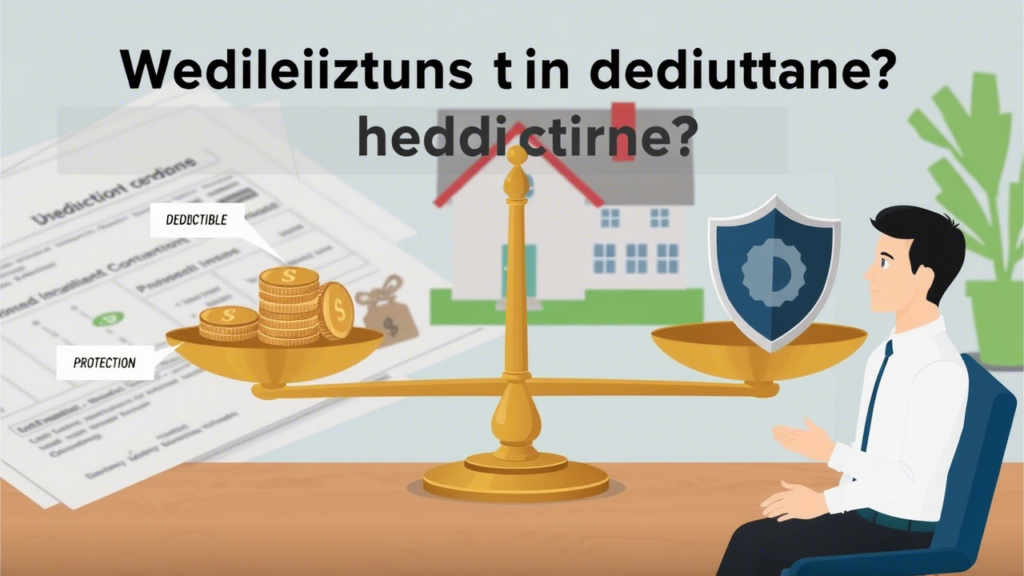

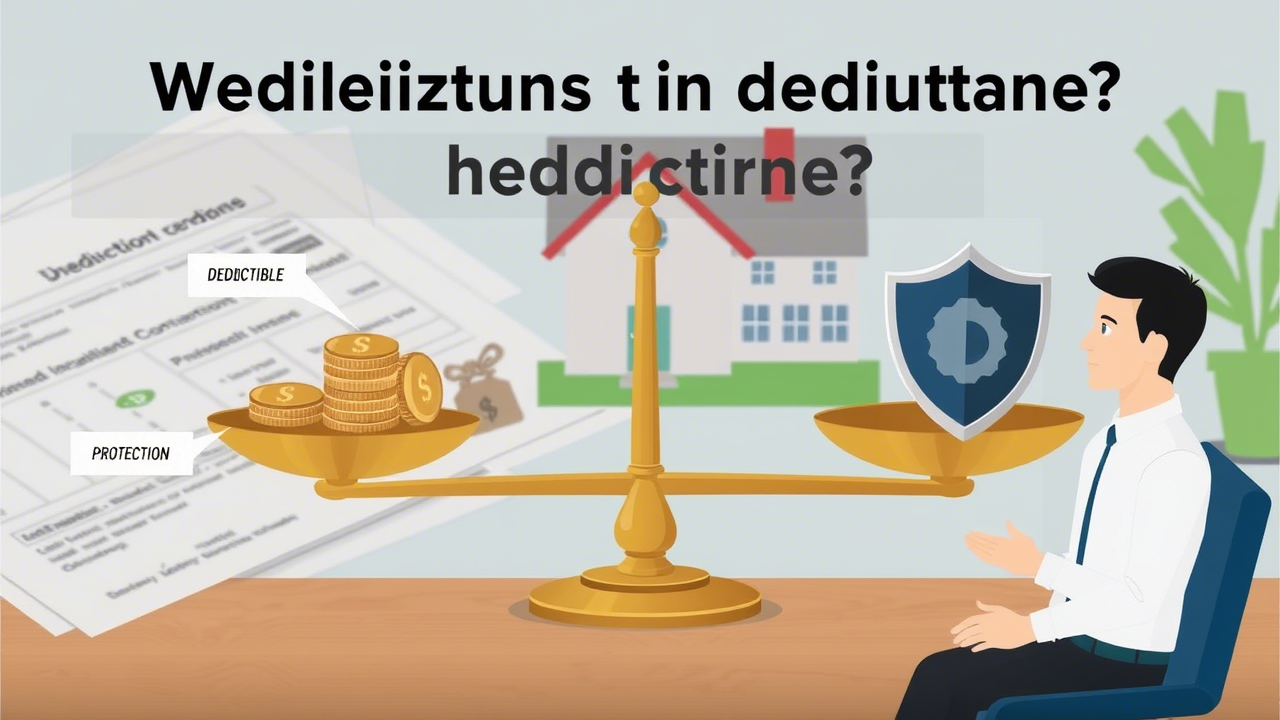

What Is a Deductible?

A deductible is the amount you agree to pay out of pocket before your insurance coverage kicks in. For example, if you have a 500deductibleonyourautoinsuranceandfileaclaimfor2,000 in repairs, you’ll pay the first 500,andyourinsurerwillcovertheremaining1,500.

Deductibles are common in many types of insurance, including:

- Health insurance

- Auto insurance

- Homeowners or renters insurance

Why Do Deductibles Exist?

At first glance, deductibles might feel like an extra financial burden. However, they serve several important purposes:

1. Encouraging Responsible Use of Insurance

Deductibles discourage policyholders from filing small, frequent claims, which can drive up costs for insurers—and, ultimately, premiums for everyone. By requiring you to cover a portion of the expense, insurers ensure that claims are reserved for more significant losses.

2. Balancing Premium Costs

Choosing a higher deductible usually means paying a lower monthly premium, while a lower deductible typically comes with higher premiums. This trade-off allows policyholders to customize their coverage based on their financial situation and risk tolerance.

3. Reducing Fraudulent Claims

Since policyholders share in the cost of a claim, deductibles help deter exaggerated or false claims, keeping insurance systems more efficient and affordable for all.

How to Choose the Right Deductible

Selecting the right deductible depends on your financial comfort level and how much risk you’re willing to assume. Here are a few considerations:

- High Deductible (Lower Premiums): A good choice if you have emergency savings and prefer lower monthly costs.

- Low Deductible (Higher Premiums): Ideal if you’d rather pay more upfront for predictable out-of-pocket costs when filing a claim.

A balanced approach is key. Assess your budget, how often you’ve needed to file claims in the past, and your ability to cover unexpected expenses.

Final Thoughts

Deductibles aren’t just a way for insurers to save money—they’re a fundamental part of how insurance maintains fairness and sustainability. By understanding how they work, you can make more informed decisions about your coverage and find a policy that aligns with your needs.

Next time you review your insurance, take a moment to consider your deductible. A little awareness today can lead to greater peace of mind tomorrow.

Would you like help evaluating your current deductible? Feel free to reach out to your insurance provider—they’re there to help you navigate these choices with confidence.